It usually takes a merger four months from the date of announcement to closure. In 95% of cases, deals with a definitive merger agreement are successfully consummated but the remaining 5% are the reason that merger arbitrage is also known as risk arbitrage. We are reminded of the risk in risk arbitrage as we write this tonight with the FTC deciding a few hours ago to sue to block the merger of luxury goods company Capri (CPRI) with Tapestry (TPR), the company that owns brands like Coach and Kate Spade.

In a few cases, companies have to navigate through stormy skies to reach their goal, and one such company that succumbed to this turbulence was Spirit Airlines. Just like we did with iRobot (IRBT) two months ago, this is our second deal postmortem. The goal of this series of articles is to provide investors with a play-by-play of how failed deals unfolded over a period of months or even years (the saga to acquire the insurance company Genworth Financial lasted four years). Deal postmortems combined with a list of all failed mergers over the last 13 years, will hopefully help arbitrageurs identify patterns and improve their odds of success with this strategy.

In the context of how the acquisition of Spirit Airlines by JetBlue (JBLU) played out, the company’s stock symbol “SAVE” was a red herring, a cry for help, a warning of impending doom.

The Bidding War

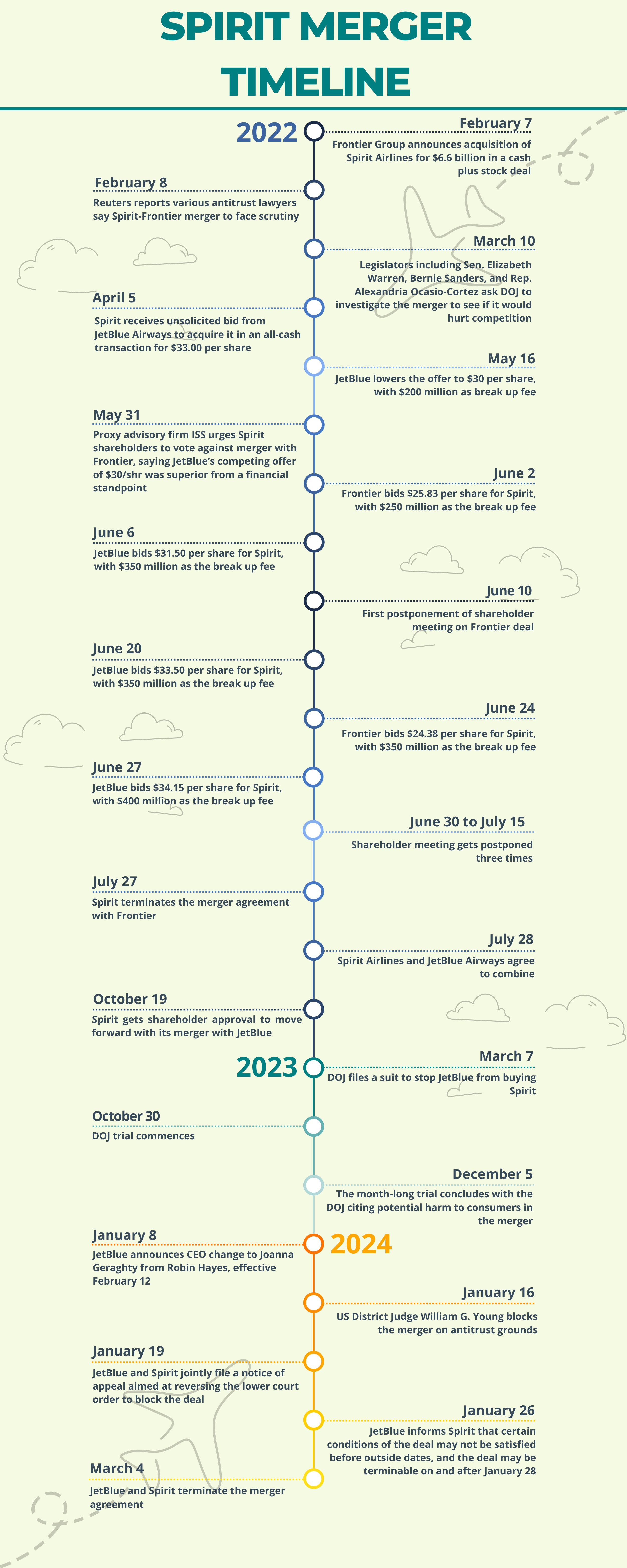

The whole saga began with a bidding war around two years ago and concluded in a legal battle which resulted in the merger falling apart.

On February 7, 2022, Denver, Colorado-based budget carrier Frontier Group Holdings (ULCC) announced that it was acquiring Florida-based Spirit Airlines for $6.6 billion in a cash plus stock deal, at a premium of 19% over the $21.73 closing price of Spirit during the prior trading session.

Spirit’s merger with Frontier was expected to create a big player in the ultra-low-cost carrier segment, but this also rang alarm bells for regulators. The U.S. Justice Department had been asked by Senators Elizabeth Warren, and Bernie Sanders, and Representative Alexandria Ocasio-Cortez to look into the merger to see if it would hurt competition.

Despite the potential regulatory challenges the deal faced, Spirit received an unsolicited proposal from another budget carrier, JetBlue Airways to acquire all of the outstanding shares of Spirit’s common stock in an all-cash transaction for $33.00 per share. This started the bidding war for the Florida-based budget carrier that lasted seven rounds.

During its bidding for Spirit, JetBlue was “highly confident” that it would secure regulatory approval for the deal. The carrier had said that while it expected a lengthy regulatory process, it was counting on its track record of lowering fares and increasing competition to get the nod.

Spirit in the first few rounds had rejected JetBlue’s offers because it had feared that the deal had a low likelihood of winning approval from government regulators. Spirit had even urged its shareholders to reject the hostile bid from JetBlue saying it was “a cynical attempt to disrupt” its merger with Frontier.

Spirit Airlines CEO, Ted Christie, had been the CFO of Frontier for seven years from 2002 to 2009 and that could point to why Spirit favored a deal with Frontier over JetBlue.

After multiple rounds of back and forth, JetBlue emerged as the winner and entered into a definitive merger agreement with Spirit Airlines to create a national low-fare challenger to the dominant big four airlines in the US. The legacy carriers, or the “Big Four” airlines, i.e., American Airlines (AAL), Delta Air Lines (DAL), Southwest Airlines (LUV), and United Airlines (UAL), control nearly 80% of the U.S. passenger market. The combined Spirit and JetBlue airline was expected to have a fleet of 458 aircraft and an order book of over 300 Airbus aircraft with fuel-efficient, low-carbon new engine options, or neo, engines.

That was just the end of the beginning of this saga. The companies reached an agreement but they still had a long way to go with regulatory approvals before the merger could come to fruition.

Regulatory Turbulence

Six months after the announcement, Spirit had shareholder approval to move forward with its deal, and it required regulatory approvals from antitrust agencies like the Federal Trade Commission (FTC) or the U.S. Department of Justice (DOJ), the Federal Aviation Administration (FAA), and the Department of Transportation.

After the Boards of both the companies had approved the merger, the companies announced that starting January 2023 till closing, the Spirit shareholders would receive $0.10 per month as a “ticking fee” which would be deducted from the termination fee based on the total value paid. During the time the companies were going through the regulatory process, Spirit shareholders were receiving 10 cents per month from JetBlue.

The DOJ, in March 2023, filed a suit to stop JetBlue from buying Spirit, saying the planned $3.8 billion merger “will lead to higher fares and fewer seats, harming millions of consumers on hundreds of routes”, calling the merger “presumptively illegal”.

Attorney General Merrick Garland said Spirit’s internal documents show that when it enters a market, fares fall by 17% while JetBlue’s internal documents show that when Spirit stops flying a route, fares go up by 30%. “The merger of JetBlue and Spirit would result in higher fares and fewer choices for tens of millions of travelers, with the greatest impact felt by those who rely on what are known as ultra-low-cost carriers to fly,” Garland had said.

After multiple delays, the trial began on October 30 where various arguments were raised for blocking the deal.

‘Raise Fares’ Argument:

The government contended that acquiring Spirit would enable JetBlue to eliminate a significant low-fare competitor, potentially reducing choices and increasing fares for consumers. JetBlue plans to remove seats from Spirit planes and shift focus to competing with major carriers.

‘Spirit Effect’ Concern:

The government argued that losing Spirit, a major disruptor with low fares, to JetBlue may lead to higher fares and increase the risk of price coordination among airlines. The “Spirit effect,” where Spirit’s entry forces other carriers to compete with lower prices, would be lost.

JetBlue’s Financial Strain:

JetBlue’s CEO testified that the airline would need to borrow $3.5 billion for the deal, potentially limiting its ability to respond to economic changes and invest in the business. The government suggests that JetBlue may become less disruptive post-merger.

Spirit’s Initial Concerns:

Initially, Spirit shared concerns with the government, fearing JetBlue would eliminate its low-fare model. Spirit’s CEO testified that JetBlue’s plan indicated a shift away from the low-cost carrier model, prompting concerns about antitrust challenges.

Divestiture Dispute:

JetBlue’s proposal to sell Spirit assets at four major airports to other carriers was contested by the government, which argued it may not guarantee similar routes. The government also raised concerns about market replacement for Spirit.

Overlapping Markets Issue:

The government asserted that the merger would grant JetBlue unfair market power due to the significant overlap in markets with Spirit. JetBlue and Spirit argue for a national market assessment, while the government insisted on evaluating local markets.

No Jury, Bench Trial:

The trial was a bench trial, with US District Judge William G. Young presiding. There was no jury, and the judge was to determine whether the sale should proceed.

When the trial was going on, competitor airlines expressed their views in favor of the merger. United Airlines CEO Scott Kirby had thought there was a 60-40 chance that the JetBlue-Spirit merger would close. Kirby had told a The Points Guy reporter that he wasn’t worried about the potential newly merged competitor: “I think we’re going to win no matter what.”

This sentiment did not sway the judge in the case.

The trial ended a little over a month later on December 5, 2023. The DOJ argued potential harm to consumers in the merger, while JetBlue asserted that it boosts competition. The judge contemplated conditional approval with extra divestitures but the DOJ was not keen on playing ball.

U.S. District Judge William Young, an 83-year-old Republican appointee, on January 16, 2024, blocked the proposed acquisition on antitrust grounds. “The government has demonstrated that consumers value Spirit flights as a unique, economical product option,” Young wrote. “The removal of Spirit as an option for consumers, therefore, would constitute a cognizable harm.”

“Spirit is a small airline. But there are those who love it. To those dedicated customers of Spirit, this one’s for you. Why? Because the Clayton Act, a 109-year-old statute requires this result — a statute that continues to deliver for the American people,” Young said in the 109-page ruling.

The Aftermath

Soon after the ruling came out, the airlines asked for an expedited appeal aimed at reversing the lower court order to block the deal. The airlines in a joint court filing asked the First U.S. Circuit Court of Appeals to reverse the decision that they argued “disregards the benefits of the transaction to the majority of the flying public.” The airlines said that if the appeal was not expedited, the court may not have an opportunity to review the decision because the merger agreement includes an outside closing date of July 24.

The U.S. appeals court did agree to hear their arguments in June, with the companies’ initial brief on February 26, the Justice Department response set for April 11, and the case to be fully briefed by April 25, 2024.

But before they could reach their appeals date, JetBlue and Spirit announced on March 4, 2024, that the airlines had decided to terminate the merger agreement. In a joint statement, the companies said that they mutually agreed that “terminating is the best path forward for both companies as required closing conditions, including receiving necessary legal and regulatory approvals, were unlikely to be met by the merger agreement’s outside date of July 24, 2024”.

“We believed this merger was worth pursuing because it would have unleashed a national low-fare, high-value competitor to the Big Four airlines,” said Joanna Geraghty, the newly appointed chief executive officer of JetBlue.

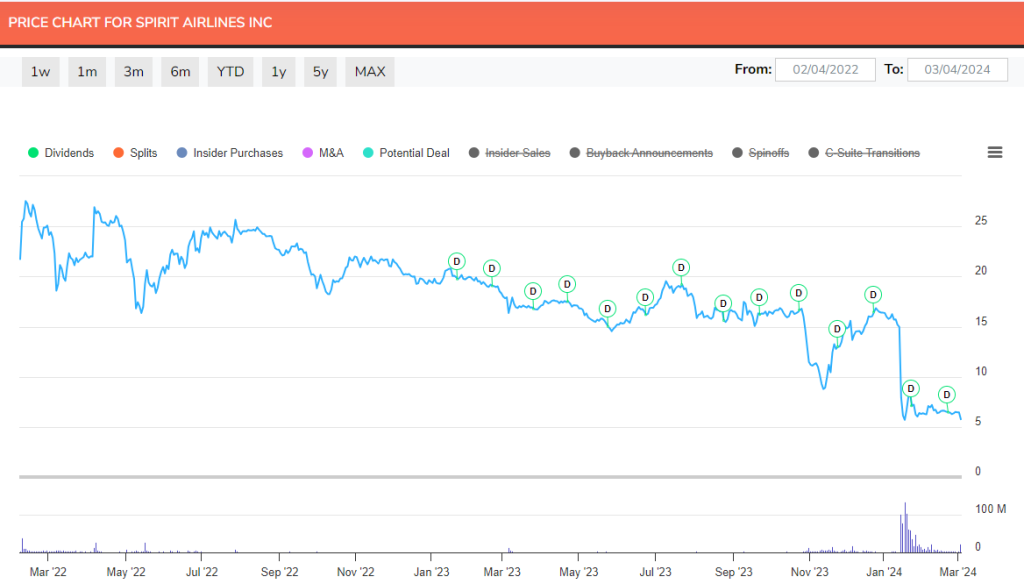

Even after all this back and forth first between Frontier and JetBlue and then between JetBlue and the DOJ, the company that got hurt the most was Spirit which saw its stock price crash to $5.76, after the deal was terminated, a 73.5% decrease from its price of $21.73 on February 4, 2022, before the whole saga started.

Key Learnings

Source: InsideArbitrage

Editor’s Note: Baranjot Kaur contributed to this article.

Disclaimer: I hold long positions in Spirit Airlines (SAVE) and Capri (CPRI). Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.